MARKET INSIGHTS

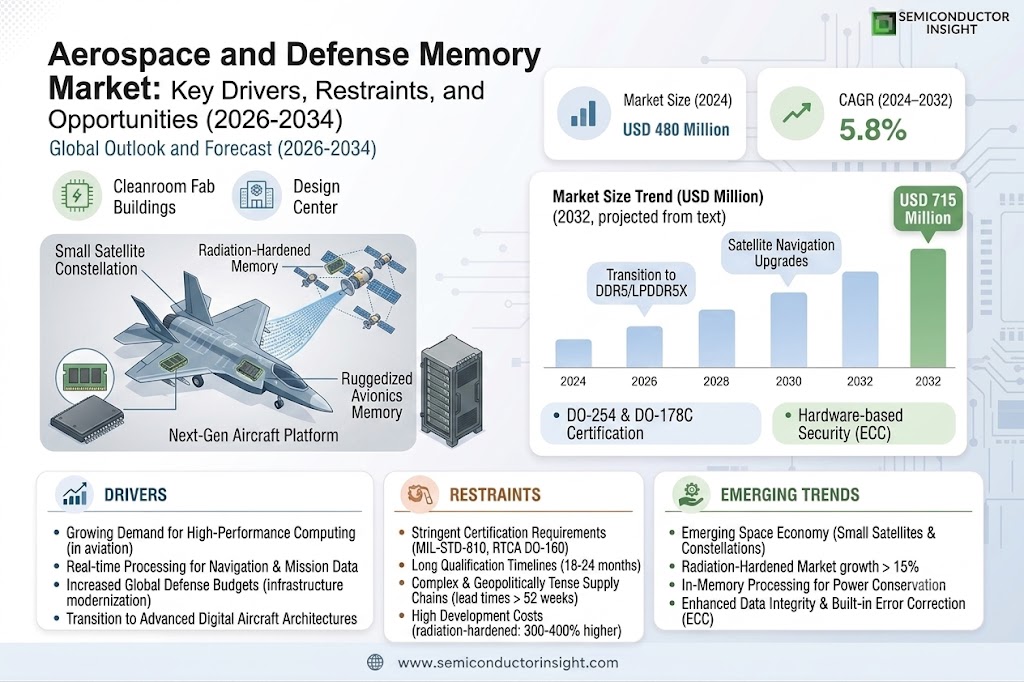

The global Aerospace and Defense Memory Market was valued at 480 million in 2024 and is projected to reach US$ 715 million by 2032, at a CAGR of 5.8% during the forecast period.

Aerospace and defense memory refers to high-performance storage solutions designed for mission-critical applications in aviation and military systems. These specialized memory components feature radiation-hardened designs, extended temperature tolerance, and enhanced reliability to withstand harsh operating environments. Key product categories include DRAM, SRAM, and non-volatile memory solutions optimized for flight control systems, satellite communications, and defense electronics.

Market growth is driven by increasing defense budgets worldwide, particularly in North America and Asia-Pacific, coupled with rising demand for unmanned aerial systems. The U.S. remains the largest market, accounting for over 40% of global demand, while China shows the fastest growth trajectory. Technological advancements in artificial intelligence and edge computing for defense applications are creating new opportunities for high-bandwidth memory solutions. Leading manufacturers like Micron, Honeywell, and Infineon continue to innovate with radiation-tolerant designs to meet evolving military and aerospace requirements.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Performance Computing in Aviation to Accelerate Market Expansion

The aerospace and defense sector is witnessing an increasing reliance on advanced computing systems for navigation, communication, and mission-critical operations. With modern aircraft and defense systems generating vast amounts of data requiring real-time processing, the demand for high-speed, ruggedized memory solutions has surged dramatically. Flight control systems in next-generation aircraft require memory solutions with read/write speeds exceeding 10GB/s and latency under 10 nanoseconds to maintain operational safety. Memory technologies like DDR5 and LPDDR5X are being rapidly adopted to meet these stringent performance benchmarks while reducing power consumption by up to 30% compared to previous generations.

Increased Defense Budgets Worldwide to Strengthen Market Position

Global military expenditure has reached unprecedented levels, with major nations allocating significant portions to modernize their defense infrastructure. This budgetary expansion directly benefits the aerospace and defense memory market as modern warfare increasingly depends on data-centric systems. Unmanned aerial vehicles (UAVs), which rely heavily on advanced memory solutions for autonomous operations and real-time data processing, are seeing production increases of 18-22% annually across leading defense manufacturers. Satellite communication upgrades and space exploration initiatives are further driving demand for radiation-hardened memory solutions capable of withstanding extreme environmental conditions.

Transition to Next-Generation Aircraft Platforms to Sustain Demand Growth

Aerospace manufacturers are actively developing new commercial and military aircraft platforms with advanced digital architectures. These next-generation systems require memory solutions that comply with stringent DO-254 and DO-178C certification standards while offering enhanced security features. The commercial aviation sector alone is projected to require over 40,000 new aircraft in the next two decades, each equipped with sophisticated avionics systems containing multiple high-performance memory modules. Memory solutions with built-in error correction (ECC) and hardware-based security are becoming standard requirements to ensure data integrity and protection against cyber threats in flight-critical systems.

MARKET RESTRAINTS

Stringent Certification Requirements to Temporarily Limit Market Penetration

The aerospace and defense sector imposes rigorous certification processes on all electronic components, creating significant barriers to entry for memory solution providers. Obtaining necessary certifications like MIL-STD-810 and RTCA DO-160 often requires 18-24 months of extensive testing and validation, delaying time-to-market for new products. These certification processes can increase development costs by 35-45% compared to commercial-grade memory solutions. For suppliers without established certification expertise, the lengthy approval timelines and substantial investment required can deter market participation, particularly for smaller manufacturers.

Complex Supply Chain Dynamics to Challenge Production Consistency

The specialized nature of aerospace-grade memory solutions creates unique supply chain challenges. Many components require dedicated production lines with enhanced quality control measures, limiting manufacturing flexibility. Geopolitical tensions and export controls have further complicated the procurement of specialized materials, with lead times for certain memory products extending beyond 52 weeks. These constraints are particularly impactful for defense applications where product lifecycle management often spans decades, requiring long-term component availability guarantees that strain existing supply chain models.

High Development Costs to Restrict Innovation Pace

Designing memory solutions that meet aerospace and defense requirements requires substantial R&D investment, with development costs for radiation-hardened memory technologies often exceeding standard commercial memory development by 300-400%. The need for extensive qualification testing across extreme temperature ranges (-55°C to 125°C) and radiation environments adds significant expense. This financial burden slows the adoption of newer memory technologies in aerospace applications, as manufacturers must carefully balance performance improvements against certification risks and development timelines.

MARKET OPPORTUNITIES

Emerging Space Economy to Create New Growth Frontiers

The rapidly expanding commercial space sector presents substantial opportunities for specialized memory solutions. Small satellite constellations and deep space missions require memory components that combine high density with extreme environmental tolerance. The radiation-hardened memory market is projected to benefit significantly from increased space exploration initiatives, with demand growing at compound annual rates exceeding 15%. Memory solutions featuring in-memory processing capabilities are gaining particular attention for space applications where minimizing data transmission is critical for power conservation.

Advancements in Memory Security to Open New Application Areas

Growing cybersecurity threats in defense systems are driving demand for memory solutions with enhanced protection features. Hardware-based security mechanisms like physical unclonable functions (PUFs) and memory encryption are being increasingly integrated into aerospace-grade memory products. The market for secure memory solutions in defense applications is expanding as military agencies implement stricter data protection standards. Memory technologies that can provide authenticated access controls while maintaining real-time performance characteristics are well-positioned to capture this emerging market segment.

Modular Avionics Architectures to Enable Scalable Solutions

The transition to open architecture avionics systems presents opportunities for memory manufacturers to develop standardized, scalable solutions. Modular designs based on standards like SOSA (Sensor Open Systems Architecture) are gaining traction, requiring memory components that support flexible configuration and future upgrades. This shift enables memory providers to offer platform-agnostic solutions that can be deployed across multiple aircraft programs, reducing development costs and accelerating adoption timelines. The ability to provide customizable memory solutions that meet varying performance, security, and environmental requirements will be critical for capitalizing on this trend.

AEROSPACE AND DEFENSE MEMORY MARKET TRENDS

Increasing Demand for High-Performance Memory in Next-Gen Defense Systems

The aerospace and defense sector is witnessing a surge in the adoption of advanced memory solutions due to the growing complexity of modern defense applications. High-reliability memory components, such as radiation-hardened DRAM and SRAM, are becoming indispensable for mission-critical systems, including flight control, satellite communications, and unmanned aerial vehicles (UAVs). The global Aerospace and Defense Memory market is projected to grow from $480 million in 2024 to $715 million by 2032, reflecting a 5.8% CAGR over the forecast period. This growth is primarily driven by the escalating need for real-time data processing and enhanced cybersecurity in military applications.

Other Trends

Advancements in Radiation-Hardened Memory Technologies

Radiation-hardened memory solutions are gaining prominence as space exploration and satellite deployments increase. Traditional memory modules face operational challenges in high-radiation environments, leading to innovations like error-correcting code (ECC) memory and custom-designed radiation-tolerant chips. Manufacturers are investing heavily in developing memory solutions capable of withstanding extreme conditions, with the DRAM segment expected to dominate market demand over the next six years. The U.S. remains the largest market, followed by increasing investments in Europe and Asia-Pacific as countries enhance their aerospace and defense capabilities.

Shift Towards AI-Integrated Memory Solutions for Autonomous Systems

The integration of artificial intelligence (AI) in defense systems is accelerating the need for high-speed, low-latency memory architectures. UAVs, autonomous drones, and next-generation fighter jets rely on AI-driven decision-making, necessitating high-bandwidth memory (HBM) and non-volatile RAM for rapid data processing. Defense contractors are collaborating with semiconductor firms to develop secure, AI-optimized memory solutions that can handle complex neural network computations while maintaining data integrity in harsh environments. Furthermore, increasing defense budgets in countries like the U.S., China, and India are fueling demand for such advanced memory technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Competition

The global Aerospace and Defense Memory Market features a competitive landscape with both established semiconductor giants and specialized manufacturers vying for market share. Micron Technology currently leads the sector, leveraging its extensive portfolio of radiation-hardened memory solutions and strategic contracts with defense contractors worldwide. The company’s success stems from decades of experience in developing high-reliability memory for extreme environments.

Following closely, Infineon Technologies and Honeywell Aerospace have strengthened their positions through continuous R&D investments in secure memory architectures. These companies recently unveiled new radiation-tolerant memory modules specifically designed for satellite and UAV applications, showcasing their technical edge in this demanding sector.

The market also sees growing competition from emerging players like ATP Electronics and RunSafe Security, who specialize in cyber-secure memory solutions for defense applications. These companies differentiate themselves through innovative approaches to data integrity and protection against sophisticated cyber threats – a critical requirement for modern military systems.

List of Key Aerospace and Defense Memory Companies

- Micron Technology, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Honeywell Aerospace (U.S.)

- NXP Semiconductors (Netherlands)

- ATP Electronics (Taiwan)

- AMD (Advanced Micro Devices) (U.S.)

- Microchip Technology (U.S.)

- Cadence Design Systems (U.S.)

- Green Mountain Semiconductor (U.S.)

- Nexus Industrial Memory (U.K.)

Segment Analysis:

By Type

DRAM Segment Leads Due to High-Speed Data Processing Capabilities in Aerospace Applications

The market is segmented based on type into:

- DRAM

- Subtypes: DDR4, DDR5, and others

- SRAM

- Flash Memory

- Subtypes: NOR Flash, NAND Flash, and others

- MRAM

- Others

By Application

Flight Control and Navigation Systems Segment Drives Adoption for Real-Time Data Processing

The market is segmented based on application into:

- Flight Control and Navigation Systems

- Communication Systems

- Defense Information Systems

- UAVs and Autonomous Systems

- Others

Regional Analysis: Aerospace and Defense Memory Market

North America

North America dominates the aerospace and defense memory market, driven by substantial investments from the U.S. Department of Defense (DoD) and private aerospace manufacturers. The U.S. accounts for the largest market share, with defense budgets exceeding $800 billion in 2024, allocating significant funds to modernize avionics, communication systems, and unmanned systems. Key players such as Micron, Honeywell, and Microchip Technology operate extensively here, emphasizing ruggedized memory solutions for harsh aerospace environments. The proliferation of DRAM-based applications, particularly in real-time flight control and navigation systems, is accelerating demand. However, stringent export controls and regulatory compliance for defense-grade memory chips pose challenges for suppliers.

Europe

Europe’s aerospace and defense memory market is propelled by collaborative defense programs like the European Defence Fund (EDF), which mandates advanced memory solutions for next-gen fighter jets and satellite systems. Countries such as France, Germany, and the U.K. leverage expertise from firms like Infineon and NXP to develop radiation-hardened memory for space applications. The region prioritizes SRAM technologies for mission-critical systems due to their low latency. Despite strong R&D investments, dependence on U.S.-based suppliers for certain high-end memory modules remains a constraint, prompting calls for greater regional self-sufficiency.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market, with China and India driving demand through indigenous defense programs and urbanization-driven aerospace expansions. China’s $230 billion defense budget in 2024 supports advancements in radar and UAV memory systems, with firms like H2TC and Huawei focusing on proprietary memory architectures. Meanwhile, India’s push for ‘Atmanirbhar Bharat’ (self-reliance) fuels local production, though reliance on imports for cutting-edge DRAM persists. Southeast Asian nations are gradually adopting aerospace memory solutions for commercial aviation, albeit with cost-conscious procurement strategies.

South America

South America’s aerospace and defense memory market remains nascent, with Brazil leading through partnerships with Airbus and Embraer. The region’s focus is on cost-effective, legacy memory modules for aging aircraft fleets, given budget constraints. Limited local manufacturing capabilities force reliance on North American and European suppliers, slowing adoption of advanced memory technologies. However, Brazil’s recent defense modernization initiatives indicate potential for gradual growth.

Middle East & Africa

The Middle East is emerging as a strategic market, with the UAE and Saudi Arabia investing heavily in defense electronics. Saudi Vision 2030’s aerospace ambitions, including the ‘SAMIKA’ initiative, demand high-reliability memory for surveillance and missile systems. While Africa’s adoption is minimal, partnerships with foreign OEMs for UAV deployments in agriculture and security signal long-term opportunities. The region struggles with fragmented supply chains but benefits from geopolitical spending on defense modernization.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Aerospace and Defense Memory markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Aerospace and Defense Memory market was valued at USD 480 million in 2024 and is projected to reach USD 715 million by 2032, growing at a CAGR of 5.8%.

- Segmentation Analysis: Detailed breakdown by product type (DRAM, SRAM, Others), application (Flight Control, Communication Systems, Defense Information Systems, UAVs), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is a key contributor, while China shows significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Honeywell, Infineon, Micron, NXP, and Microchip Technology, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of radiation-hardened memory solutions, high-speed data processing capabilities, and integration with next-gen aerospace systems.

- Market Drivers & Restraints: Evaluation of defense budget allocations, space exploration programs, and cybersecurity requirements versus supply chain challenges and certification complexities.

- Stakeholder Analysis: Strategic insights for memory component manufacturers, aerospace OEMs, defense contractors, and technology providers.

The analysis combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Aerospace and Defense Memory Market?

-> Aerospace and Defense Memory Market was valued at 480 million in 2024 and is projected to reach US$ 715 million by 2032, at a CAGR of 5.8% during the forecast period.

Which key companies operate in this market?

-> Major players include Honeywell, Infineon, Micron, NXP, Microchip Technology, AMD, and Cadence Design Systems.

What are the key growth drivers?

-> Growth is driven by increasing defense expenditures, space exploration programs, and demand for high-reliability memory in critical aerospace applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is emerging as the fastest-growing region.

What are the emerging trends?

-> Key trends include radiation-hardened memory solutions, AI integration for autonomous systems, and advanced packaging technologies for aerospace applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...