MARKET INSIGHTS

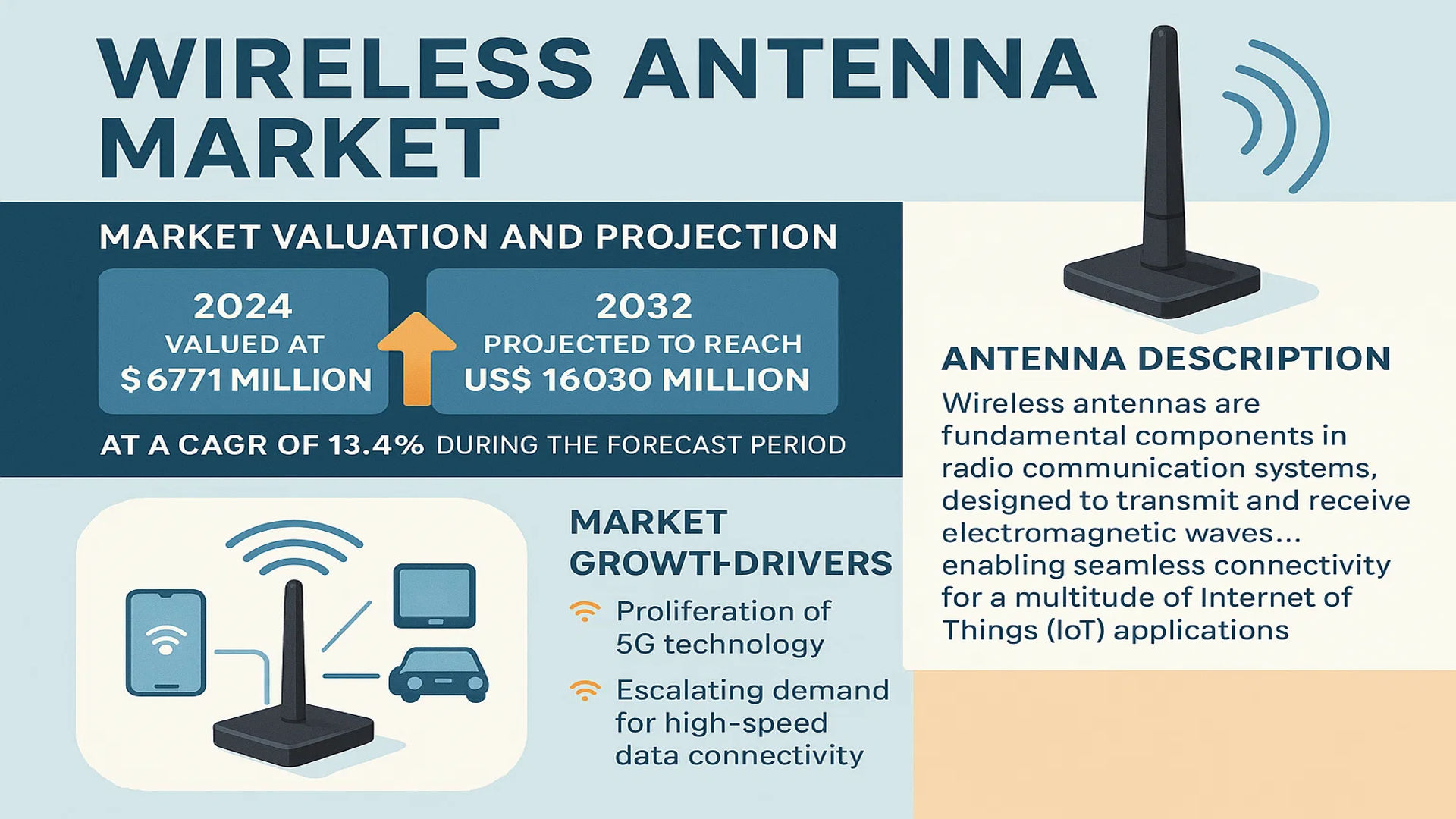

The global Wireless Antenna Market was valued at 6771 million in 2024 and is projected to reach US$ 16030 million by 2032, at a CAGR of 13.4% during the forecast period..

Wireless antennas are fundamental components in radio communication systems, designed to transmit and receive electromagnetic waves. They are integral to Wi-Fi networking, functioning by sending and picking up radio transmissions on specific frequencies. These antennas can be either externally mounted or embedded within the hardware enclosure of devices such as routers, smartphones, laptops, tablets, wearables, and automotive systems, enabling seamless connectivity for a multitude of Internet of Things (IoT) applications.

The market is experiencing robust growth driven by the proliferation of 5G technology, escalating demand for high-speed data connectivity, and the exponential expansion of the IoT ecosystem. Furthermore, the increasing adoption of smart devices and advancements in automotive telematics are significant contributors to market expansion. The competitive landscape is dynamic, with the top five manufacturers collectively holding approximately 40% of the global market share. Geographically, the Asia-Pacific region dominates, accounting for about 80% of the market, followed by North America and Europe. Key players such as Harada, Amphenol, and Molex continue to innovate and expand their portfolios to capture growth opportunities in this rapidly evolving sector.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G Infrastructure and IoT Devices to Accelerate Market Expansion

The global deployment of 5G networks represents a fundamental driver for the wireless antenna market, with over 300 commercial 5G networks launched worldwide as of early 2024. This massive infrastructure expansion requires advanced antenna systems capable of supporting higher frequency bands, massive MIMO (Multiple Input Multiple Output) configurations, and beamforming technologies. The transition to 5G has necessitated antenna designs that can operate across low-band, mid-band, and high-band spectrum ranges, creating substantial demand for sophisticated antenna solutions. Additionally, the Internet of Things ecosystem continues to expand rapidly, with projections indicating more than 30 billion connected IoT devices by 2025, each requiring specialized antenna systems for reliable connectivity across diverse applications including smart cities, industrial automation, and connected vehicles.

Growing Consumer Electronics Market and Automotive Connectivity Demands

The consumer electronics sector continues to drive significant antenna demand, with smartphone shipments exceeding 1.4 billion units annually and the wearable technology market growing at approximately 15% CAGR. Modern smartphones now incorporate multiple antennas for cellular connectivity (supporting 4G LTE and 5G), Wi-Fi 6/6E, Bluetooth, GPS, and NFC functionalities, creating complex antenna system requirements. The automotive sector represents another major growth area, with connected car shipments projected to reach 76 million units by 2025. Advanced driver assistance systems (ADAS), vehicle-to-everything (V2X) communication, and in-vehicle infotainment systems all require specialized antenna solutions, driving innovation in automotive antenna designs and integration techniques.

Technological Advancements in Antenna Design and Materials

Recent breakthroughs in antenna technology are significantly enhancing performance while reducing size and power consumption. The development of metamaterials and advanced composite substrates has enabled the creation of antennas with improved efficiency and broader bandwidth capabilities. Innovations in antenna design, including the adoption of phased array systems and adaptive beamforming technologies, are particularly crucial for 5G applications where signal directionality and network capacity are paramount. Furthermore, the integration of artificial intelligence for antenna optimization and the emergence of reconfigurable intelligent surfaces are opening new possibilities for dynamic signal management and network efficiency improvements across various wireless applications.

MARKET CHALLENGES

Miniaturization and Integration Complexities in Compact Device Designs

The relentless push toward smaller, thinner, and more powerful electronic devices creates significant engineering challenges for antenna designers. As device form factors shrink, available space for antennas diminishes, requiring innovative solutions that maintain performance while occupying minimal physical volume. The proximity of multiple antennas within compact devices often leads to signal interference and performance degradation, necessitating advanced isolation techniques and sophisticated tuning algorithms. Additionally, the integration of metallic components and other RF-obstructive materials in modern device designs further complicates antenna placement and performance optimization, requiring extensive simulation, prototyping, and testing cycles that increase development costs and time-to-market.

Other Challenges

Performance Consistency Across Environmental Conditions

Maintaining consistent antenna performance across varying environmental conditions remains a persistent challenge. Factors such as temperature fluctuations, humidity, physical obstructions, and user handling can significantly impact antenna efficiency and radiation patterns. The performance variability becomes particularly critical in automotive and IoT applications where devices must operate reliably in diverse and often harsh environmental conditions. Ensuring consistent connectivity across these variable conditions requires robust design approaches, extensive environmental testing, and sometimes redundant antenna systems, all of which contribute to increased complexity and cost.

Regulatory Compliance and Certification Complexities

Navigating the complex landscape of global regulatory requirements presents substantial challenges for antenna manufacturers. Different regions have varying certification standards for RF emissions, frequency allocations, and wireless performance metrics. The certification process for new antenna designs can be time-consuming and expensive, particularly when addressing multiple international markets simultaneously. Additionally, the rapid evolution of wireless standards means that regulatory requirements are constantly changing, requiring ongoing compliance monitoring and potential design modifications to meet updated standards across different geographical markets.

MARKET RESTRAINTS

High Development Costs and Technical Complexity Limiting Market Entry

The wireless antenna market faces significant barriers to entry due to the substantial research and development investments required for advanced antenna technologies. Developing cutting-edge antenna solutions involves sophisticated electromagnetic simulation tools, extensive testing equipment, and highly specialized engineering expertise. The complexity of modern antenna systems, particularly those supporting multiple frequency bands and advanced technologies like beamforming, requires multidisciplinary teams with expertise in RF engineering, materials science, and signal processing. These technical and financial barriers make it challenging for new entrants to compete effectively with established players who have accumulated decades of experience and substantial intellectual property portfolios in antenna design and manufacturing.

Supply Chain Vulnerabilities and Component Shortages

The global nature of the electronics supply chain introduces significant vulnerabilities that can restrain market growth. Recent disruptions have highlighted the fragility of component availability, with semiconductor shortages and logistics challenges affecting antenna production schedules and costs. The specialized materials required for high-performance antennas, including certain substrate materials and conductive elements, often come from limited sources, creating potential supply bottlenecks. Additionally, fluctuations in raw material prices and geopolitical factors affecting international trade can impact manufacturing costs and lead times, making consistent production planning challenging and potentially delaying product launches in the highly time-sensitive consumer electronics and telecommunications markets.

Standardization Issues and Interoperability Challenges

The absence of universal standards across certain wireless technologies creates interoperability challenges that can restrain market growth. While major cellular standards are well-established, emerging technologies and proprietary implementations in IoT and specialized industrial applications often lack complete standardization. This fragmentation requires antenna manufacturers to develop multiple product variants to address different technical specifications and performance requirements. The need to support backward compatibility with older wireless standards while incorporating new technologies further complicates antenna design, often resulting in performance compromises or increased complexity. These standardization challenges can slow adoption rates in certain market segments where interoperability across different systems and generations of technology is essential.

MARKET OPPORTUNITIES

Emerging Applications in Satellite Communication and Non-Terrestrial Networks

The rapid expansion of satellite communication systems and non-terrestrial networks presents substantial growth opportunities for advanced antenna technologies. With multiple low-earth orbit satellite constellations being deployed, the demand for ground segment antennas capable of tracking moving satellites and maintaining stable connections is increasing significantly. The emerging direct-to-device satellite communication market, which aims to provide connectivity directly to standard smartphones, requires innovative antenna solutions that can operate effectively with satellite systems while maintaining compatibility with terrestrial networks. This convergence of satellite and terrestrial connectivity is driving development of hybrid antenna systems and creating new market segments with substantial growth potential through the latter half of the decade.

Advancements in Smart Antenna Systems and AI-Driven Optimization

The integration of artificial intelligence and machine learning into antenna systems opens new opportunities for performance optimization and operational efficiency. Smart antenna systems capable of automatically adapting to changing environmental conditions, network demands, and usage patterns are becoming increasingly feasible. These intelligent systems can optimize signal strength, reduce interference, and extend battery life in mobile devices through dynamic configuration adjustments. The application of AI algorithms for antenna design optimization is also reducing development time and improving performance outcomes. These technological advancements are creating opportunities for premium antenna solutions that offer superior performance and energy efficiency, particularly in high-value applications such as premium smartphones, automotive systems, and critical infrastructure communications.

Expansion into New Industrial and Medical Applications

Beyond traditional consumer and telecommunications applications, wireless antennas are finding new opportunities in industrial automation, healthcare, and specialized commercial applications. The industrial IoT sector requires robust antenna solutions capable of operating in challenging environments with high reliability requirements. Medical applications, including remote patient monitoring and wireless medical devices, demand antennas with specific performance characteristics and regulatory compliance. The growing adoption of wireless technology in agricultural automation, smart infrastructure, and environmental monitoring is creating additional market segments with specialized antenna requirements. These emerging applications often command higher margins and present opportunities for antenna manufacturers to develop specialized products tailored to specific industry needs and operational environments.

WIRELESS ANTENNA MARKET TRENDS

Proliferation of 5G Infrastructure Deployment to Emerge as a Dominant Trend

The global rollout of 5G networks is fundamentally reshaping the wireless antenna landscape, driving unprecedented demand for advanced antenna systems. This transition necessitates a massive upgrade from traditional 4G infrastructure, requiring antennas capable of supporting higher frequencies, massive MIMO (Multiple Input Multiple Output) technology, and beamforming capabilities. The number of 5G connections worldwide is projected to exceed 2 billion by 2025, a figure that underscores the immense scale of this infrastructure build-out. This expansion is not limited to consumer mobile devices; it is also critical for enabling low-latency communication for industrial IoT, autonomous vehicles, and smart city applications. Consequently, antenna manufacturers are innovating at a rapid pace to develop smaller, more efficient, and highly integrated antenna solutions that can meet the stringent performance requirements of 5G networks, including operation in both sub-6 GHz and millimeter-wave spectrum bands.

Other Trends

Integration of Antennas in IoT and Automotive Applications

The explosive growth of the Internet of Things (IoT) and the advancement of connected and autonomous vehicles are creating substantial new revenue streams for the wireless antenna market. Billions of IoT devices, from smart sensors to wearables, each require reliable wireless connectivity, often in challenging form factors and environments. Similarly, modern vehicles are evolving into sophisticated connected platforms, integrating multiple antennas for cellular connectivity (C-V2X), GPS, satellite radio, Wi-Fi, and ADAS (Advanced Driver-Assistance Systems) radar. This trend demands antennas that are not only highly performant but also seamlessly integrated into device housings and vehicle designs, leading to increased adoption of antenna designs like flexible printed circuits (FPCs) and laser-direct structuring (LDS) technology to save space and improve aesthetics.

Advancements in Material Science and Antenna Design

Innovation in materials and design methodologies is a key trend propelling the market forward, enabling the development of next-generation antennas that are more efficient, broadband, and compact. The use of new dielectric materials and metamaterials is allowing for the creation of antennas with enhanced gain and directionality while reducing their physical footprint. Furthermore, the industry is increasingly leveraging sophisticated simulation software and AI-driven design tools to optimize antenna performance before physical prototyping, significantly accelerating development cycles and reducing costs. This focus on R&D is crucial for meeting the evolving demands of modern wireless standards, which require antennas to support a wider range of frequencies and more complex modulation schemes without compromising on size or power consumption, particularly in space-constrained mobile devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global wireless antenna market exhibits a semi-consolidated structure, characterized by the presence of several established multinational corporations alongside numerous specialized regional manufacturers. The market’s dynamism is fueled by relentless technological advancement and the escalating demand for high-speed connectivity across consumer electronics, automotive, and IoT applications. The top five manufacturers collectively command approximately 40% of the global market share, underscoring the significant influence of leading players.

Harada Industry Co., Ltd. stands as a dominant force, particularly within the automotive antenna segment. Its leadership is anchored in long-standing supply agreements with major global automakers and a robust portfolio of advanced antenna systems for connected vehicles, including 5G and V2X (Vehicle-to-Everything) solutions. Similarly, Amphenol Corporation leverages its extensive engineering capabilities and global distribution network to secure a substantial market position, supplying antennas for a vast array of applications from mobile devices to infrastructure.

Meanwhile, companies like Molex LLC (a subsidiary of Koch Industries) and Sunway Communication are intensifying competition through significant research and development investments focused on miniaturization and enhanced performance for 5G mmWave applications. Their growth is further propelled by strategic expansions into emerging markets and securing contracts with leading smartphone OEMs. The competitive intensity is further heightened by the strategic activities of players like Skycross Inc., which is known for its innovative antenna designs that improve signal reliability in compact devices.

Furthermore, the competitive landscape is evolving as companies actively engage in mergers, acquisitions, and partnerships to broaden their technological expertise and geographic reach. This strategic maneuvering allows them to offer more integrated solutions and capture a larger share of the value chain. The focus remains on developing antennas that support the next generation of wireless technology, ensuring compatibility and performance in an increasingly interconnected world.

List of Key Wireless Antenna Companies Profiled

- Harada Industry Co., Ltd. (Japan)

- Amphenol Corporation (U.S.)

- Sunway Communication (China)

- Molex, LLC (U.S.)

- Skycross Inc. (U.S.)

- Yokowo Co., Ltd. (Japan)

- Galtronics (Canada)

- Pulse Electronics (U.S.)

- Laird Connectivity (U.K.)

- Shenglu Telecommunication Co., Ltd. (China)

Segment Analysis:

By Type

UHF Antennas Segment Leads the Market Owing to Superior Performance in Short-Range, High-Frequency Applications

The market is segmented based on type into:

- UHF (Ultra High Frequency)

- Subtypes: Whip, Panel, Yagi, and others

- VHF (Very High Frequency)

- Subtypes: Dipole, Ground Plane, and others

- Others

By Application

Mobile Devices Segment Dominates Due to Pervasive Integration in Smartphones and Tablets

The market is segmented based on application into:

- Mobile Devices

- Subtypes: Smartphones, Tablets, Laptops, Wearables

- Automotive

- IOT (Internet of Things)

- Others

By End User

Consumer Electronics Sector Holds Largest Share Fueled by Mass Production of Connected Devices

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

- Others

Regional Analysis: Wireless Antenna Market

Asia-Pacific

The Asia-Pacific region dominates the global wireless antenna market, accounting for approximately 80% of total market share. This overwhelming dominance is driven by massive manufacturing hubs in China, South Korea, and Taiwan, which produce the majority of the world’s smartphones, tablets, and IoT devices. China alone contributes significantly to both supply and demand, with local manufacturers like Sunway, Shenglu, and Inzi Controls playing pivotal roles. The region benefits from extensive 5G network deployments, particularly in countries like South Korea and Japan, which were among the first to adopt widespread 5G infrastructure. Furthermore, rapid urbanization, growing disposable incomes, and government initiatives promoting smart city projects are accelerating the adoption of connected devices. While cost sensitivity remains a factor, driving demand for both UHF and VHF antenna types, there is a clear trend toward advanced, miniaturized antennas to support next-generation applications in mobile devices and automotive sectors.

North America

North America represents a technologically advanced and high-value market, characterized by stringent performance standards and early adoption of innovations such as 5G and Wi-Fi 6/6E. The United States is the largest contributor, fueled by robust investments in telecommunications infrastructure and the presence of leading device manufacturers and tech companies. Regulatory standards set by the FCC ensure that antennas meet strict efficiency and emissions criteria. The market is also driven by high consumer demand for premium smartphones, wearables, and smart home devices. Key players like Amphenol and Molex have a strong foothold here, supplying advanced antenna solutions for automotive and IoT applications. However, the market is highly competitive, with a focus on R&D to develop antennas that support higher frequencies and greater data throughput, essential for applications in autonomous vehicles and augmented reality.

Europe

Europe’s wireless antenna market is shaped by strong regulatory frameworks, including the EU’s Radio Equipment Directive (RED), which emphasizes efficiency, safety, and interoperability. The region shows significant demand from the automotive sector, where leading manufacturers incorporate advanced antenna systems for connected car technologies, navigation, and V2X communication. Countries like Germany, France, and the UK are at the forefront, driven by investments in 5G infrastructure and IoT deployments across industrial and consumer segments. Environmental sustainability is increasingly influencing product development, with a push toward materials and designs that reduce ecological impact. While the market is mature and innovation-driven, it faces challenges from economic fluctuations and complex regulatory compliance, which can slow time-to-market for new antenna technologies compared to Asia-Pacific.

South America

South America is an emerging market with growth potential tied to expanding mobile network coverage and increasing smartphone penetration. Brazil and Argentina are the key markets, where telecom operators are gradually upgrading infrastructure to support 4G and 5G services. However, economic volatility and currency instability often hinder large-scale investments, making cost-effective antenna solutions more prevalent. The adoption of advanced antennas in automotive and IoT applications is still in early stages, limited by lower disposable incomes and infrastructure gaps. Nonetheless, government initiatives to improve digital inclusion and urban development projects are expected to drive gradual growth, particularly in mobile devices and basic IoT applications, presenting opportunities for antenna suppliers offering reliable, budget-friendly products.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by infrastructure development and increasing mobile connectivity. Gulf Cooperation Council (GCC) countries, such as Saudi Arabia and the UAE, are leading in the adoption of advanced technologies, including 5G and smart city projects, which drive demand for high-performance antennas. In contrast, Africa faces challenges related to limited infrastructure, economic constraints, and political instability, though mobile device adoption is rising rapidly. The market is characterized by a dual demand spectrum: high-end antennas for urban, tech-savvy consumers and cost-effective solutions for price-sensitive regions. While the market is not as mature as others, long-term growth is anticipated as digital transformation initiatives gain momentum and network coverage expands across the continent.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Wireless Antenna markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wireless Antenna Market?

-> Wireless Antenna Market was valued at 6771 million in 2024 and is projected to reach US$ 16030 million by 2032, at a CAGR of 13.4% during the forecast period.

Which key companies operate in Global Wireless Antenna Market?

-> Key players include Harada, Amphenol, Sunway, Molex, and Skycross, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for mobile devices, expansion of IoT applications, and automotive connectivity advancements.

Which region dominates the market?

-> Asia-Pacific is the largest market, holding approximately 80% of global market share.

What are the emerging trends?

-> Emerging trends include 5G antenna integration, miniaturization of components, and development of multi-band antennas.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...